S Ahmad

In less than a generation, India has moved from a largely cash-driven economy to one of the most sophisticated digital financial ecosystems in the world. What once required physical branches, paperwork, and long waiting periods can now be completed in seconds on a mobile phone. But the deeper transformation underway is no longer just about digitisation—it is about intelligence.

Financial inclusion in India is entering a new phase where access is no longer the primary challenge. The question now is not whether people can open bank accounts or receive money, but whether financial systems can truly understand them—accurately, fairly, and in real time. The convergence of Digital Public Infrastructure (DPI) and Artificial Intelligence (AI) is reshaping that answer.

This shift is subtle but profound. India is moving from “financial inclusion as access” to “financial inclusion as empowerment”—where credit decisions, risk assessments, fraud detection, and financial services are increasingly driven by data, algorithms, and consent-based digital ecosystems. It is a transformation that is both technical and deeply social in its consequences.

The Digital Backbone: DPI as the Foundation of Trust

Any discussion of AI in finance in India must begin with the infrastructure that makes it possible. Unlike many countries where financial digitisation evolved in fragmented silos, India built a coordinated digital backbone that now supports scale, interoperability, and trust.

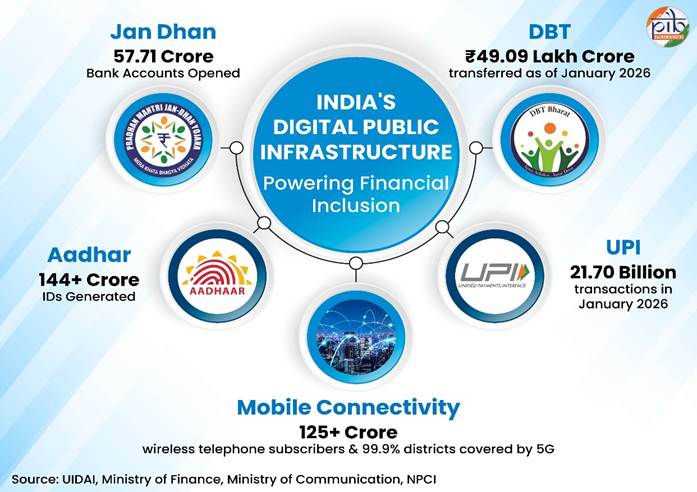

At the heart of this system is the JAM architecture—Jan Dhan, Aadhaar, and Mobile. This trinity created the first large-scale bridge between citizens and formal finance. Bank accounts brought people into the financial system, biometric identity provided authentication, and mobile connectivity enabled real-time interaction.

The impact has been extraordinary. Millions who once lived outside formal banking systems are now part of it. The expansion of Jan Dhan accounts—from a relatively limited base a decade ago to tens of crores today—represents more than a policy success; it represents a structural redefinition of citizenship in financial terms. Money is no longer mediated by geography or intermediaries. It is increasingly direct.

This foundation is reinforced by real-time payments infrastructure such as the Unified Payments Interface (UPI), developed by the National Payments Corporation of India ecosystem. UPI has transformed payments from a friction-heavy process into a seamless exchange of value. Whether it is a roadside vendor or a large retailer, transactions now occur instantly and with minimal cost.

The scale is staggering. Monthly transaction volumes run into billions, with values in tens of lakh crores. But beyond the numbers lies a more important reality: UPI has normalized digital trust. People who never used digital banking now rely on it daily. That behavioral shift is critical because AI systems depend not just on data—but on participation at scale.

Complementing this is Direct Benefit Transfer (DBT), which has fundamentally re-engineered welfare delivery. By transferring subsidies directly into bank accounts, DBT has reduced leakages, improved transparency, and strengthened state capacity. It has also generated a large, structured financial dataset that can be used—carefully and ethically—for improving governance and service delivery.

Together, JAM, UPI, and DBT have created something rare in global terms: a real-time, interoperable, population-scale financial data system.

From Digitisation to Intelligence: The AI Layer

If DPI is the nervous system of India’s financial ecosystem, AI is becoming its cognitive layer.

Artificial Intelligence is now being deployed not merely to automate processes but to interpret financial behaviour. Traditional financial systems relied heavily on static indicators such as income certificates, collateral, and credit history. These systems inherently excluded millions of individuals whose economic lives were informal, seasonal, or undocumented.

AI disrupts this limitation by enabling alternative credit assessment models. Instead of asking “Do you have a credit score?”, the system increasingly asks “What does your financial behaviour indicate?”

Digital footprints—from payments, utility bills, GST records, and account activity—are transformed into dynamic risk profiles. This is especially transformative for Micro, Small and Medium Enterprises (MSMEs), informal workers, and first-time borrowers who have historically been underserved by formal credit systems.

In economic terms, this shift is not incremental—it is structural. It potentially unlocks a credit gap estimated in the range of hundreds of billions of dollars, particularly in underserved segments. More importantly, it reduces dependence on informal lending channels that often carry high interest rates and exploitative conditions.

But this transformation is not purely technological. It depends on trust in data governance, consent mechanisms, and regulatory oversight.

Policy Architecture: Innovation with Guardrails

India’s approach to AI in financial services has been notably cautious yet ambitious. Rather than allowing unrestricted experimentation, the system has evolved through structured regulatory frameworks and institutional coordination.

One of the most significant enablers is the Regulatory Sandbox framework developed by the Reserve Bank of India. The sandbox allows fintech companies and banks to test new products under controlled conditions. This is not just a compliance mechanism—it is a learning environment where innovation and regulation evolve together.

It reflects a critical philosophy: innovation must not outpace safety, but safety must not suffocate innovation.

Another major pillar is the multilingual AI initiative led by Digital India BHASHINI Division under the BHASHINI program. India’s linguistic diversity has historically been a barrier to financial access. Millions of people are excluded not because they lack identity or income, but because they cannot navigate financial systems designed in languages they do not understand.

The “Banking BHASHINI” model aims to change that by embedding banking vocabulary, regulatory language, and customer support into multilingual AI systems. This is not merely translation—it is contextual understanding. Financial inclusion, in this sense, becomes linguistic inclusion.

By integrating speech, text, and translation datasets through initiatives like BhashaDaan, the system continuously improves its ability to serve diverse populations. In practical terms, it allows a farmer in a remote district and an urban professional to interact with financial systems in equally intuitive ways.

At the same time, fraud detection and cybersecurity are being strengthened through AI-driven systems such as MuleHunter.AI, developed by the Reserve Bank Innovation Hub. This tool uses machine learning to detect suspicious transaction patterns, particularly those associated with mule accounts used in money laundering or cybercrime.

Unlike rule-based systems, AI models can identify anomalies in real time, adapting to evolving criminal tactics. This is crucial in an environment where financial fraud is becoming increasingly sophisticated and cross-platform.

Mule accounts, frequently used to launder money and facilitate cybercrime, have consistently posed difficulties for traditional detection approaches.

Reimagining Credit: The Rise of Alternative Scoring Systems

Perhaps the most consequential transformation lies in credit systems.

For decades, access to credit in India was governed by rigid scoring mechanisms that depended on formal financial histories. This created a structural exclusion problem: those without documented credit histories were considered “high risk” by default.

AI is dismantling this assumption.

Through systems like the Unified Lending Interface (ULI), lenders can now access a wide range of structured and unstructured data sources through standardized APIs. These include authentication services, financial records, land data, and other verified datasets.

ULI is not just a technological platform—it is a new architecture of lending infrastructure. It enables frictionless credit decision-making while maintaining traceability and regulatory oversight.

Alongside ULI, the Account Aggregator framework introduced by Reserve Bank of India has further strengthened consent-based data sharing. Users can securely share financial data across institutions without repeatedly submitting documents. This reduces friction, speeds up approvals, and improves accuracy in credit underwriting.

Importantly, this system is voluntary and consent-driven. That principle is critical. Without consent, data systems risk becoming extractive. With consent, they become empowering.

Together, ULI and Account Aggregators are building the rails for AI-driven credit systems that are faster, more inclusive, and more adaptive than anything that existed before.

The Informal Economy and the Digital ShramSetu Vision

One of the most ambitious extensions of AI-led inclusion is its application to informal labour markets.

India’s informal workforce—estimated at hundreds of millions—has historically operated outside formal financial systems. The Digital ShramSetu initiative aims to bridge this gap by combining AI, blockchain, and digital skilling platforms.

The goal is not only financial inclusion but economic visibility. By creating verifiable skill records and enabling access to financial services, such systems can integrate informal workers into formal economic pathways.

This has deep implications. It transforms informal labour from an invisible segment into a measurable, credit-worthy, and policy-relevant population.

Risks, Constraints, and Ethical Questions

Despite its promise, AI-powered financial inclusion is not without risks.

First, there is the risk of algorithmic bias. AI systems trained on historical data may inadvertently reinforce existing inequalities. If past lending patterns excluded certain groups, models trained on that data may replicate those exclusions in new forms.

Second, privacy concerns are central. Consent-based systems like Account Aggregators are designed to mitigate this risk, but implementation quality matters. Weak enforcement or poor user awareness can undermine consent frameworks.

Third, over-reliance on digital footprints can create new exclusions. Individuals with limited digital activity may be unfairly assessed as high-risk, even if they are financially stable in real terms.

Fourth, explainability remains a challenge. Complex AI models can produce accurate predictions without offering transparent reasoning. In financial contexts, this can undermine trust and regulatory accountability.

These challenges do not negate the value of AI in financial inclusion—but they highlight the need for continuous governance evolution.

Account Aggregators (AAs) are NBFCs that facilitate the retrieval and consolidation of a customer’s financial information. They transfer data from one financial institution to another based on an individual’s instruction and consent.

The Road Ahead: From Inclusion to Intelligence at Scale

India’s financial ecosystem is no longer just expanding outward; it is evolving inward—becoming smarter, more adaptive, and more predictive.

The convergence of DPI and AI is creating a system where financial services are no longer reactive but anticipatory. Credit can be extended faster, fraud can be detected earlier, and services can be tailored more precisely to individual needs.

But the deeper transformation is philosophical. Financial inclusion is no longer about bringing people into the system. It is about redesigning the system itself to understand people better.

In this sense, India is not just digitising finance—it is re-architecting it.

As the country moves toward its long-term development vision, these systems will play a defining role. The success of AI-powered financial inclusion will depend not only on technological capability but on governance, ethics, and inclusivity.

If implemented responsibly, this model has the potential to become a global benchmark. It demonstrates how large, diverse, and complex societies can use digital infrastructure not just for efficiency—but for equity.

Conclusion: A New Financial Social Contract

The story of AI-powered financial inclusion in India is ultimately a story about a new social contract between citizens, institutions, and technology.

It is a contract built on data, but governed by consent. Powered by algorithms, but shaped by regulation. Driven by scale, but grounded in inclusion.

The transformation underway is not merely financial—it is civilizational in its implications. It redefines who participates in the economy, how value is assessed, and what fairness means in a digital age.

India’s journey shows that inclusion is no longer a question of access alone. It is a question of intelligence, design, and intent.

And in that shift—from access to intelligence—the future of finance is already being rewritten.

Comments are closed.