S. Ahmad

Over the past decade, India’s economic story has increasingly been shaped not just by large industries or corporate giants, but by millions of small entrepreneurs working quietly in towns, villages, and city bylanes. These micro-enterprises—tea stalls, repair shops, tailoring units, transport services, and home-based businesses—form the invisible backbone of the country’s economy. Yet, for decades, they remained outside the formal financial system, dependent on informal credit and vulnerable to exploitation.

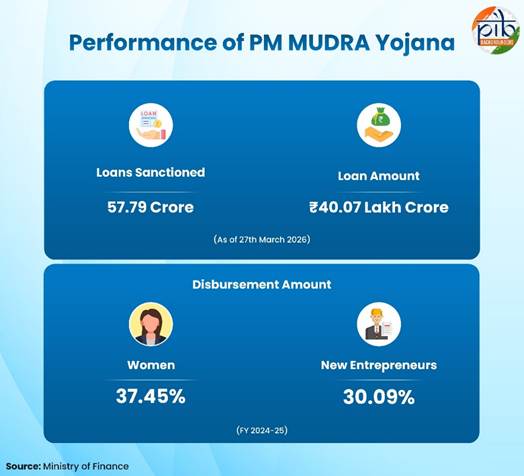

The launch of the Pradhan Mantri MUDRA Yojana (PMMY) in 2015 marked a decisive attempt to correct this imbalance. Built on the powerful idea of “Funding the Unfunded,” the scheme sought to democratize access to credit by extending collateral-free loans to micro and small enterprises. Eleven years later, its scale and impact are difficult to ignore—over 57 crore loans disbursed, amounting to more than ₹40 lakh crore. These numbers are not merely statistical milestones; they represent millions of aspirations translated into action.

At its core, PMMY is not just a credit scheme—it is a structural intervention in India’s development model. By recognizing micro-entrepreneurs as legitimate economic actors, it has shifted the narrative from job-seeking to job-creation. It has enabled individuals with limited resources but strong intent to step into the formal economy, often for the first time.

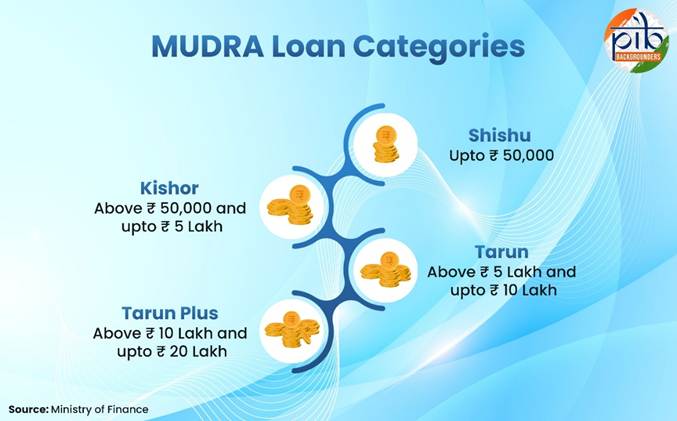

One of the most significant contributions of PMMY lies in its inclusive design. The scheme’s tiered loan structure—Shishu, Kishor, Tarun, and now Tarun Plus—ensures that businesses at different stages of growth receive appropriate financial support. A street vendor seeking ₹30,000 and a small manufacturer aiming for ₹15 lakh are both accommodated within the same framework. This flexibility reflects a deep understanding of India’s diverse entrepreneurial landscape.

Equally important is the scheme’s emphasis on accessibility. By offering collateral-free loans, PMMY has dismantled one of the biggest barriers faced by small borrowers. Traditionally, lack of assets meant exclusion from formal credit systems. MUDRA has challenged this norm, replacing collateral with trust and potential. The involvement of institutions such as banks, NBFCs, and microfinance bodies has ensured that credit reaches even the last mile.

The social impact of this initiative is particularly noteworthy. Nearly 60% of loan accounts belong to women, signalling a quiet but powerful shift toward gender-inclusive entrepreneurship. For many women, especially in rural and semi-urban areas, access to credit has meant more than just income—it has meant autonomy, confidence, and a stronger voice within households and communities.

Similarly, the participation of new entrepreneurs—accounting for around one-fifth of beneficiaries—indicates that PMMY is not merely supporting existing businesses but actively fostering new ones. This is crucial in a country where employment generation remains a pressing challenge. By enabling self-employment and small-scale enterprise growth, the scheme contributes to a more decentralized and resilient economic structure.

However, the true strength of PMMY lies not only in its scale but in its ecosystem. Over the years, the scheme has evolved into a technology-driven framework, integrating with digital platforms like the JanSamarth portal. Such integration has simplified application processes, improved transparency, and reduced delays in disbursement. Complementary mechanisms like the Credit Guarantee Fund for Micro Units have further strengthened lender confidence, ensuring that the flow of credit remains uninterrupted.

The real measure of success, however, is best seen in individual stories. Across India, beneficiaries have used MUDRA loans to transform their lives—from small traders expanding their businesses to first-time entrepreneurs building enterprises that generate employment for others. These stories reflect a broader shift in the economic psyche—from dependency to self-reliance.

Yet, it is important to approach this success with a balanced perspective. While PMMY has significantly expanded access to credit, questions around credit quality, repayment capacity, and long-term sustainability cannot be ignored. Easy access to loans must be matched with adequate financial literacy, market linkages, and business support systems. Without these, there is a risk that micro-entrepreneurs may struggle to scale or sustain their ventures.

Moreover, the next phase of the scheme must focus not just on quantity but on quality. The goal should be to help micro-enterprises evolve into stable, growth-oriented businesses. This requires a shift from mere credit provision to a more holistic support system—one that includes skill development, mentorship, and integration with larger value chains.

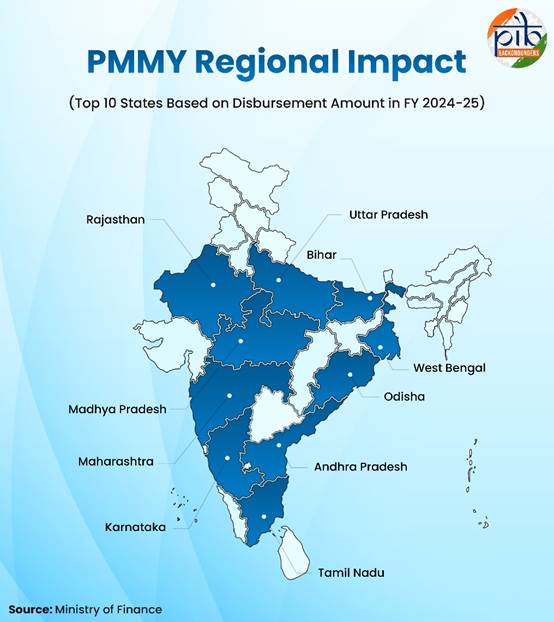

Another critical dimension is the need to address regional disparities. While states like Uttar Pradesh, Bihar, and Maharashtra have seen significant loan disbursement, ensuring balanced outreach across all regions remains essential. Tailored strategies may be required to address the unique challenges of geographically and economically diverse areas.

Despite these challenges, the achievements of PMMY over the past eleven years are undeniable. It has redefined financial inclusion by moving beyond bank accounts to actual credit access. It has empowered individuals at the margins to become active participants in economic growth. Most importantly, it has reinforced the idea that small enterprises are not peripheral—they are central to India’s development story.

As India moves toward its vision of becoming a developed economy, the role of micro-entrepreneurs will only grow in importance. Schemes like PMMY must continue to evolve, ensuring that today’s small borrowers become tomorrow’s successful business owners.

In the final analysis, the success of the MUDRA Yojana is not just about loans disbursed—it is about dignity restored, confidence built, and opportunities created. It is about recognizing that big transformations often begin with small steps.

And sometimes, all it takes to change a life is a small loan—and a chance to dream.

Comments are closed.